BADideas.fund's Positioning Problem: What 16 Baltic VC Competitors Reveal

Every fund in the Baltics claims operator experience and hands-on support. One fund has 250 operators. The rest have messaging.

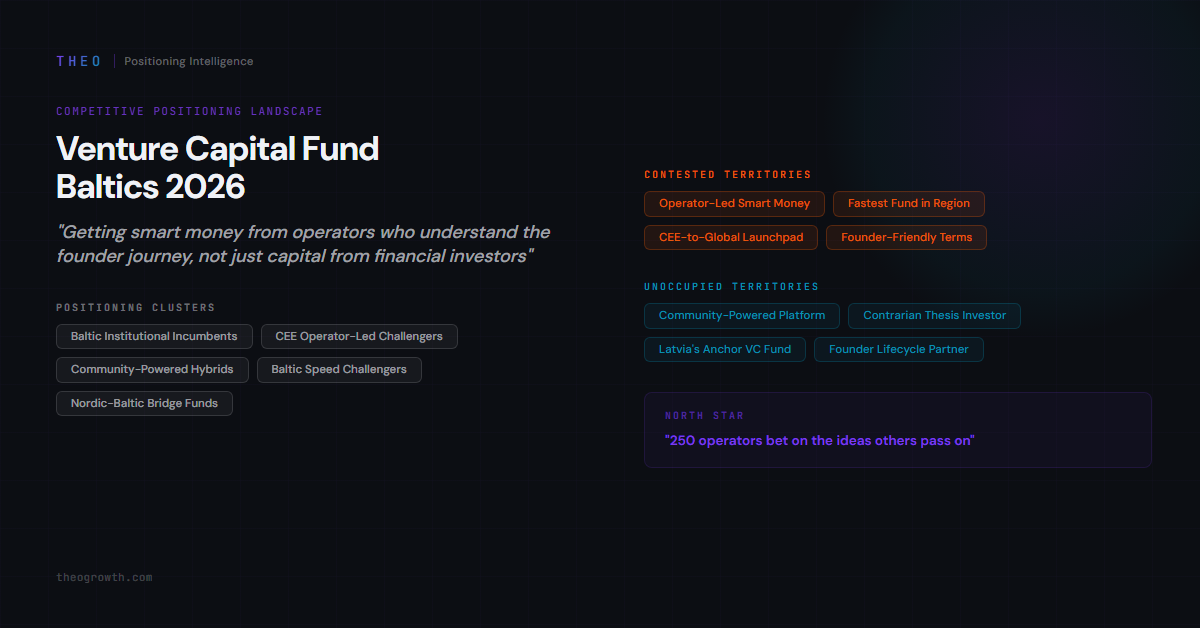

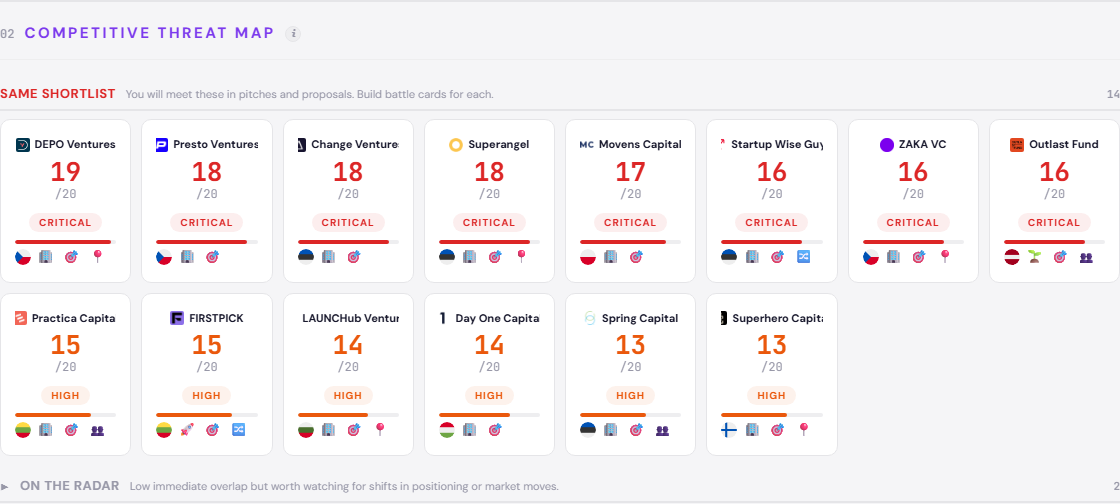

The Baltic venture capital landscape has a messaging problem disguised as a strategy problem. THEO’s discovery phase identified 57 competitors across the Baltic and CEE VC landscape. The 16 highest-priority funds - selected by relevance to BADideas.fund’s positioning - were analyzed in depth. All 16 claim hands-on operator support. Zero proves it structurally. BADideas.fund sits at the edge of this crowded field with something none of them has - a 250-member operator syndicate that co-invests deal-by-deal. The question is whether that structural difference translates into a defensible position before competitors replicate the model.

The Landscape: A Messaging Monoculture With Real Consequences

The dominant frame in Baltic VC is straightforward: buyers - founders raising pre-seed and seed rounds - evaluate funds through a single lens. “Getting smart money from operators who understand the founder journey, not just capital from financial investors.” Every fund in this landscape has internalized that frame. The problem is what they did with it.

Half the analyzed landscape competes directly for the same positioning territory as BADideas.fund - targeting the same founders, communicating the same operator-led narrative, claiming the same hands-on support. DEPO Ventures is the closest structural mirror - it runs an identical hybrid fund-plus-syndicate model with a CEE focus and scores 19 on the positioning threat index, the highest in the landscape. Presto Ventures, Change Ventures, and Superangel all target the same buyer segment with overlapping operator-led claims. Movens Capital competes for the same CEE operator-led positioning with a EUR 60M fund advantage. The remaining 8 target adjacent buyers with overlapping claims but less direct positioning overlap. Every analyzed fund poses significant competitive pressure - none occupy a distant or unrelated positioning.

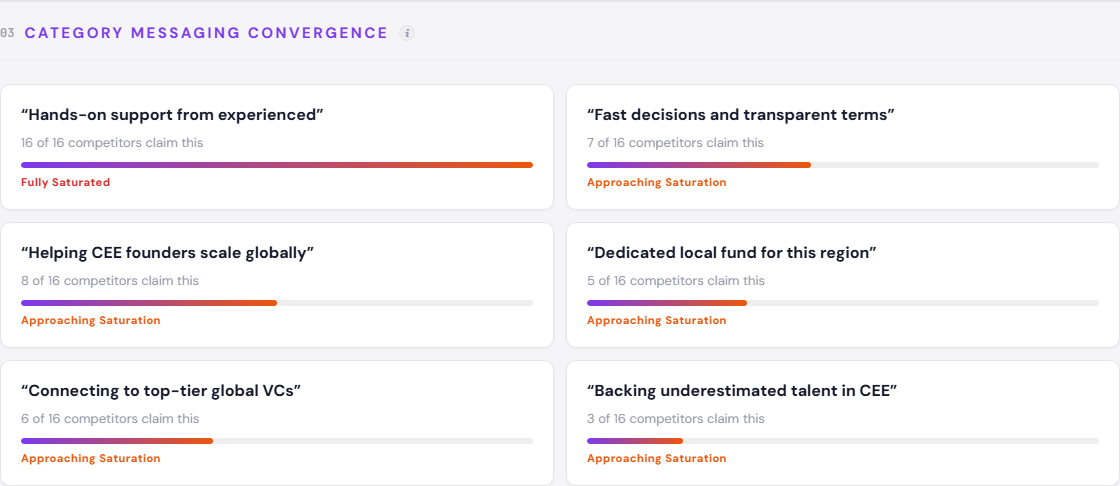

The convergence data tells the real story. “Hands-on support from experienced operators” - 16 of 16 analyzed competitors claim this. Full saturation. Not approaching it, not trending toward it. Every analyzed fund says the same thing. “Helping CEE founders scale globally” - 8 of 16. “Fast decisions and transparent terms” - 7 of 16. BADideas.fund overlaps with all three of these saturated zones.

This is what a messaging monoculture looks like in practice. When every fund claims operator experience, the claim stops functioning as differentiation and starts functioning as table stakes. CEE founders raising their first institutional round hear the same pitch 16 times. The funds that win aren’t the ones with the best version of this pitch - they’re the ones who escape it entirely.

This analysis is based on the Venture Capital Fund Competitive Positioning Landscape we published for BADideas.fund. The full interactive report - with every competitor’s threat score, territory claims, and strategic reasoning - is available to explore here.

Where BADideas.fund Stands

BADideas.fund occupies the EDGE of the Community-Powered Hybrids cluster - a group of three funds running syndicate-style models alongside traditional fund structures. The other two members of this cluster operate similar hybrid approaches, but with smaller communities and weaker brand differentiation. Internal competition within the cluster is MEDIUM, which means the positioning overlap is real but not yet destructive.

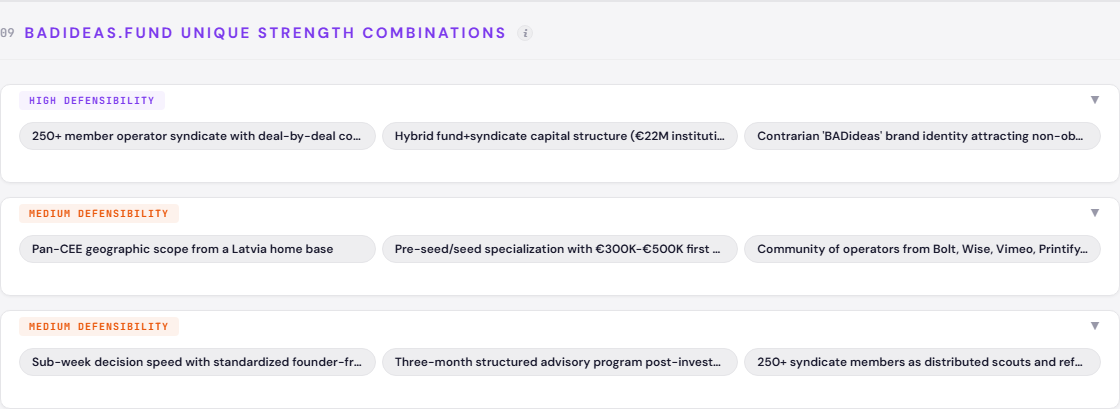

The structural advantage is specific. BADideas.fund has 250-plus operators who co-invest deal-by-deal. This is not an advisory board. This is not a mentor network. This is capital deployment through a community of builders from Bolt, Wise, Vimeo, Printify, and Shopify who put money into every deal alongside the fund. No competitor has framed their syndicate as a platform - all describe it as a feature. That distinction matters.

Three assumption gaps favor the fund. First, no competitor has claimed the “Community-Powered Investment Platform” territory - it sits unoccupied with HIGH client fit. Second, among the 16 analyzed, none have embraced a contrarian thesis identity. All target “ambitious” or “exceptional” founders. None embrace non-obvious bets. The BADideas brand name is already doing this work - it just needs strategic amplification. Third, among the 16 analyzed, only 2 are Latvia-based compared to 5-plus from Estonia. “Latvia’s Anchor VC Fund” is an unoccupied territory with HIGH client fit.

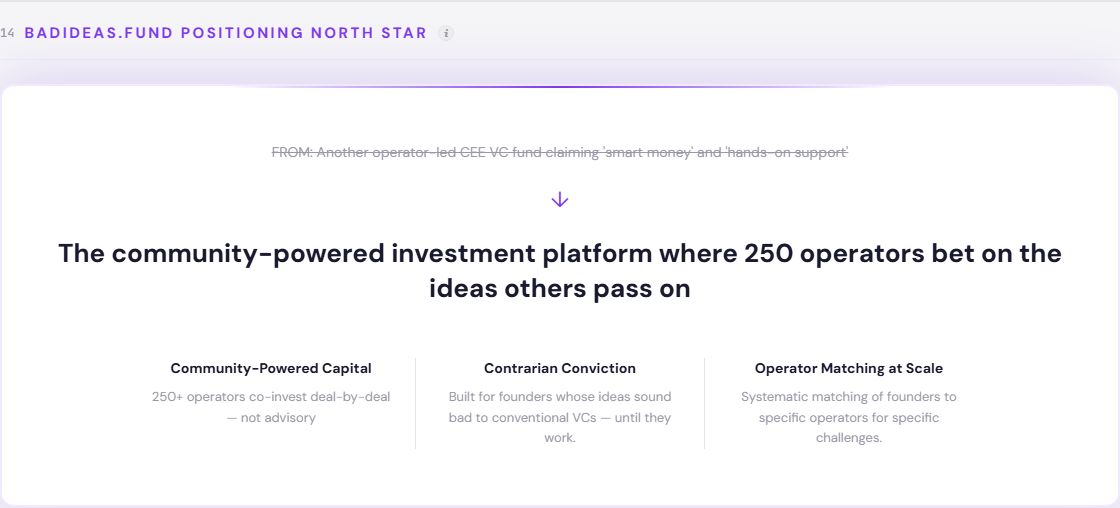

The north star direction moves the fund from “another operator-led CEE VC fund claiming smart money and hands-on support” to “the community-powered investment platform where 250 operators bet on the ideas others pass on.” Three pillars support this: Community-Powered Capital (250-plus operators co-investing deal-by-deal), Contrarian Conviction (built for founders whose ideas sound bad until they work), and Operator Matching at Scale (systematic matching of founders to specific operators for specific challenges).

Five Clusters, Three Forks, and the Hybrid Model Risk

The 16 competitors organize into five positioning clusters. The Baltic Institutional Incumbents - Practica Capital, Spring Capital, and Day One Capital - trade on fund size and track record. Practica manages EUR 80M, Day One EUR 60M. The CEE Operator-Led Challengers cluster has HIGH internal competition - three funds fighting over the same “operators who became investors” positioning. The Baltic Speed Challengers cluster has LOW internal competition, suggesting that speed-based positioning still has room.

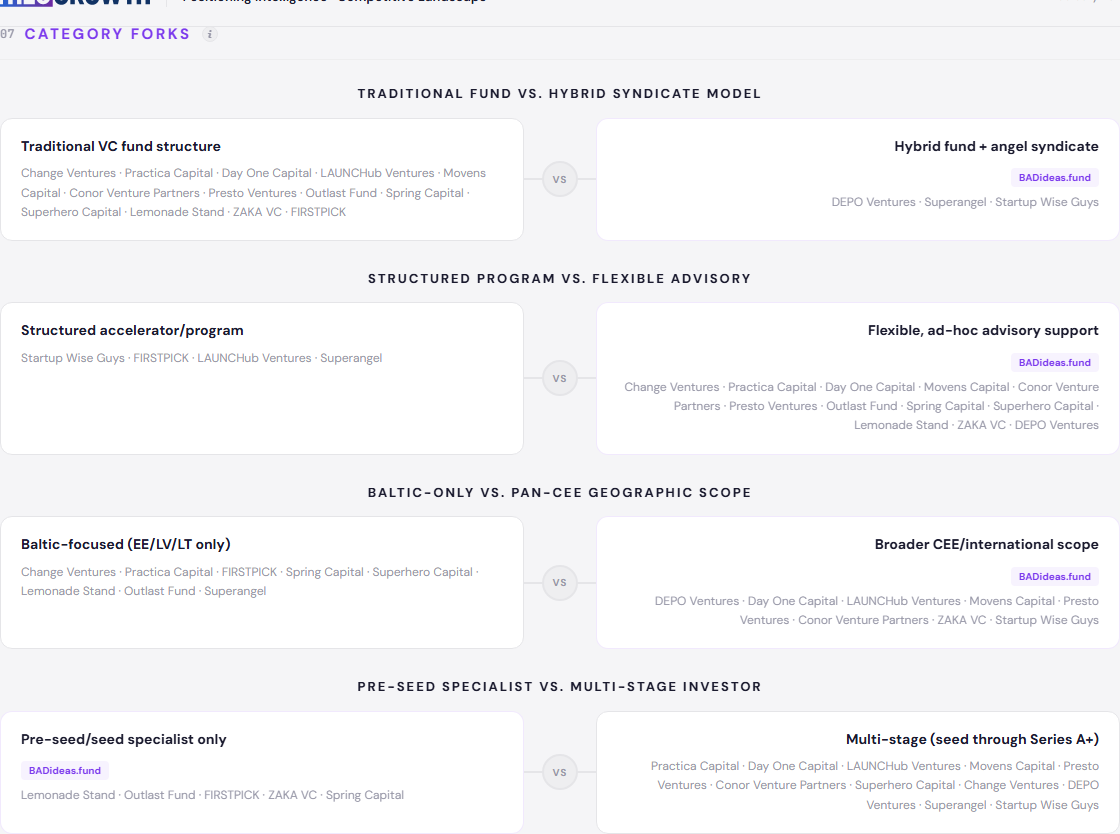

The most consequential structural fork: Traditional Fund versus Hybrid Syndicate Model. BADideas.fund sits on the Hybrid side with only DEPO Ventures, Superangel, and Startup Wise Guys. 13 competitors sit on the Traditional side. This is a meaningful structural bet - the fund is in the minority position on the most important category tension.

An emerging category frame deserves attention. “Patient capital for durable companies, not hype-chasing quick exits” is still NASCENT - no dominant champion yet. “Transatlantic bridge connecting CEE talent to US market access” is EMERGING, with ZAKA VC and Outlast Fund already building credibility in this space. If the transatlantic bridge frame matures, it could pull deal flow away from regionally-focused funds.

The risk that demands monitoring: hybrid syndicate models getting replicated by competitors. BADideas.fund’s structural advantage - the 250-member community - took years to build. But the model itself is visible and understood. If DEPO Ventures - already the closest structural mirror with an identical hybrid model and the highest positioning threat index score in the landscape - scales its own community to comparable size, BADideas.fund’s differentiation narrows to brand and contrarian thesis alone. The fund size disadvantage compounds this - Practica at EUR 80M, Day One at EUR 60M, and Movens Capital at EUR 60M can absorb the cost of building community infrastructure that a smaller fund cannot match.

When 16 of 16 competitors claim operator experience, the only defensible move is to prove it structurally - not say it louder.

What This Means: Strategic Implications

The path forward has three layers: what to own now, what to reframe, and what to build.

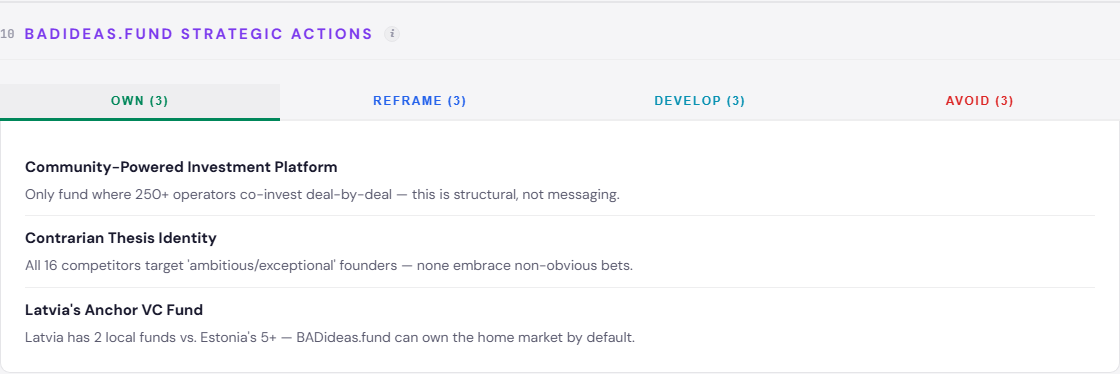

Own immediately: The Community-Powered Investment Platform territory is unoccupied and has HIGH client fit. No competitor has framed their syndicate this way. The Contrarian Thesis Identity - “backing founders others underestimate” instead of “backing ambitious CEE founders” - is equally open. Latvia’s Anchor VC Fund positioning fills a geographic gap that Estonia’s crowded fund landscape cannot contest.

Reframe the saturated claims. “Hands-on support from operators” becomes “250 operators is greater than 3 partners.” “Institutional track record” becomes “recent operator experience is more valuable than fund vintage.” “Largest fund in the region” becomes “right-sized for pre-seed is better than biggest fund.” These reframes don’t abandon the operator narrative - they make it structural and verifiable.

Develop forward-looking capabilities. The Operator Matching Engine - systematic matching of founders to specific operators for specific challenges - is HIGH priority. This transforms the community from a capital source into a service platform. Portfolio Performance Transparency and Cross-Portfolio Customer Introductions are MEDIUM priority but build the “platform” narrative.

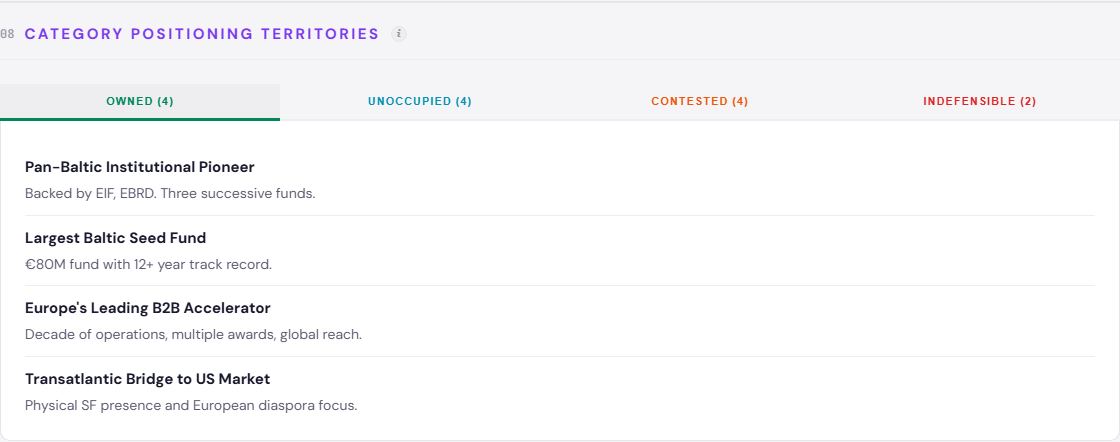

Avoid at all costs: “Hands-On Support Beyond Capital” (every competitor claims this), “Backing Ambitious CEE Founders” (8-plus use identical messaging), and “Pan-Baltic Institutional Pioneer” (Change Ventures owns this territory). Competing in these spaces means spending resources to say what everyone already says.

The monitoring signal is DEPO Ventures. It is the closest structural mirror in the landscape - same hybrid model, same CEE focus, same operator narrative. If DEPO scales its community past 100 members or rebrands around a contrarian thesis, BADideas.fund’s window to own these territories narrows significantly.

The Bottom Line

BADideas.fund has a structural asset that no competitor matches - 250 operators deploying capital deal-by-deal. The strategic failure would be describing that asset in the same language every other fund uses. The positioning work is not about finding a better adjective for “hands-on support.” It is about making the community the product, the contrarian thesis the filter, and the platform the category - before DEPO Ventures figures out the same playbook.

Explore the full BADideas.fund positioning landscape analysis - interactive competitor analysis, territory maps, and strategic actions: available here.

1 The positioning threat index is a 0-20 composite score measuring four dimensions: Ecosystem Reach, Messaging Convergence, Category Overlap, and Trajectory Threat. Each dimension is weighted and scored from competitor intelligence data. A score above 15 is classified Critical.

2 Client fit is assessed on three criteria: whether the brand already has operational capabilities to credibly claim the territory, whether the territory aligns with the brand’s current market position and buyer expectations, and whether competitive pressure makes the territory strategically urgent. HIGH means all three criteria are met.

3 All competitor data is sourced from publicly available information: company websites, published pricing pages, press releases, news coverage, and credible third-party sources (Crunchbase, industry analyst reports, LinkedIn company profiles). No proprietary or confidential data was used. This analysis contains three layers: observed facts (what competitors publicly communicate and claim), analytical interpretation (how we classify and score those observations using our framework), and strategic recommendations (what we suggest the focus brand should do). Scores, cluster assignments, and territory classifications are our analytical interpretation of public data - not statements of objective market truth. Strategic actions (OWN, REFRAME, DEVELOP, AVOID) are recommendations, not predictions.

This analysis was produced using THEO Growth - positioning intelligence for brand strategists. If you work with brands and need competitive positioning analysis, see how it works.