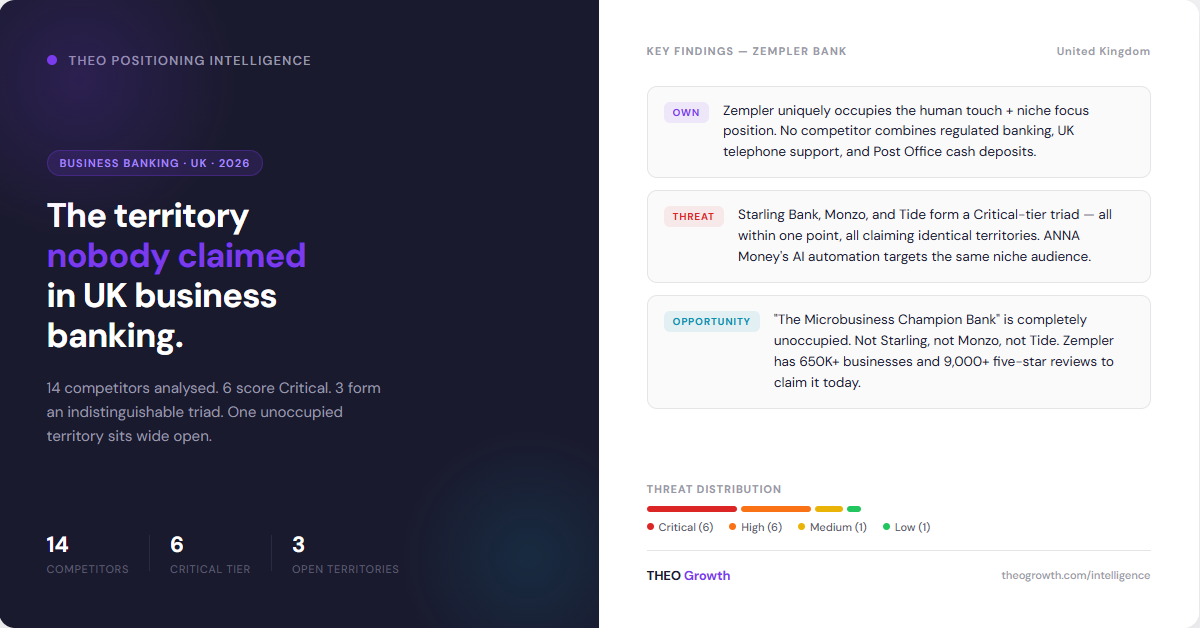

Zempler Bank's Positioning Problem: What 14 UK Business Banking Competitors Reveal

Six score Critical threat level. Three form an indistinguishable triad. And the most valuable territory in the landscape is sitting completely unclaimed.

Zempler Bank operates in one of the most commoditised corners of UK financial services. Six of the fourteen competitors it faces score Critical on the positioning threat index. The top three - Starling Bank, Monzo, and Tide - are functionally indistinguishable from a messaging perspective. And yet, buried inside this crowded landscape, there are three positioning territories that nobody has claimed. Zempler holds the keys to all of them.

The Landscape: A Six-Way Critical Pile-Up

UK business banking for SMEs and microbusinesses has a structural problem: the challengers all sound the same.

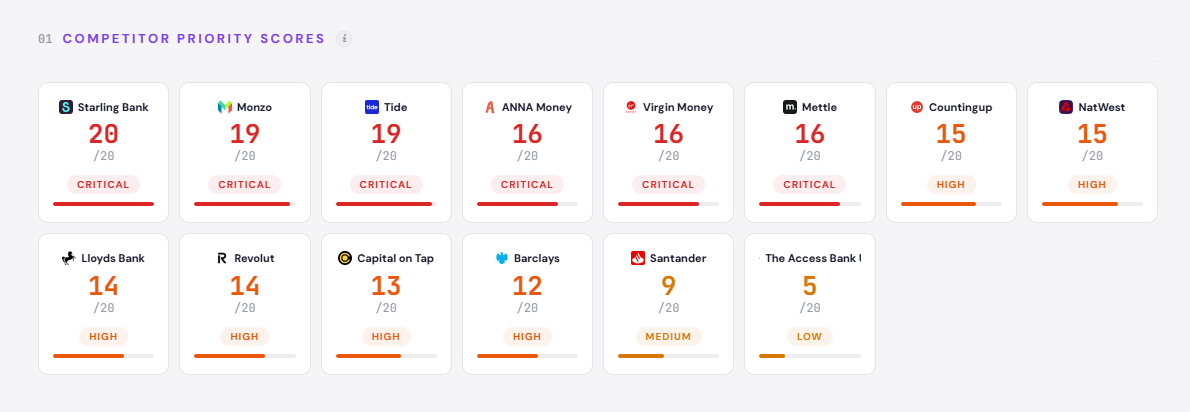

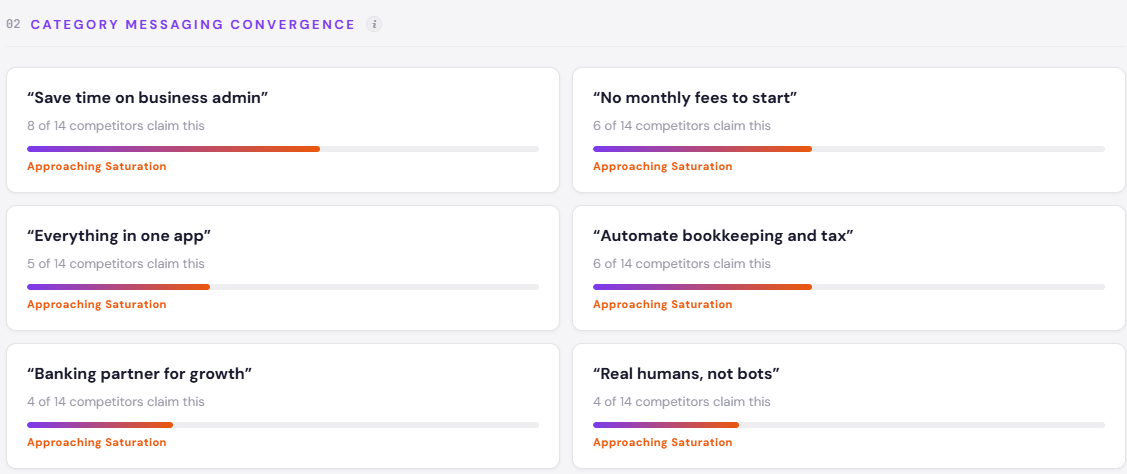

Starling Bank leads the threat index at 20 - the maximum score. Monzo and Tide both score 19. ANNA Money, Virgin Money, and Mettle all score 16. That’s six competitors at Critical threat level, separated by just four points across the entire tier. From a positioning perspective, this is not a competitive landscape — it’s a messaging monoculture. Every one of these brands claims some version of “simpler business banking,” “everything in one app,” or “save time on admin.” Eight of the fourteen competitors make the “save time on business admin” claim. Six offer a free account. Five promise “everything in one app.”

The result is a market where the loudest voices are saying the same thing, and the differentiation that does exist is buried in feature lists rather than brand identity.

Below the Critical tier, the landscape spreads out. Countingup and NatWest score 15 (High tier), followed by Lloyds Bank, Revolut, and Capital on Tap at 14. Barclays sits at 12. Santander drops to 9. The Access Bank UK scores just 5 — a specialist in African trade finance that barely registers as a business banking competitor for Zempler’s audience.

The full interactive positioning landscape is available here — every competitor’s threat score, territory claims, and strategic reasoning.

Where Zempler Bank Stands

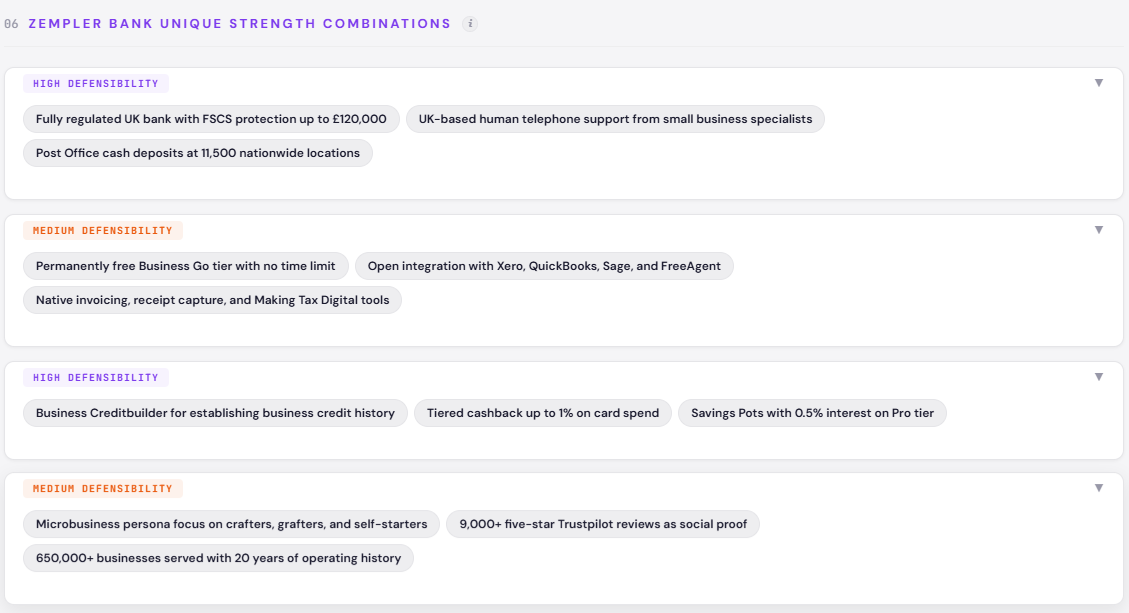

Zempler occupies an interesting position in this landscape: high digital simplicity, focused banking scope, and a human-first service model. On the Digital Simplicity vs. Service Breadth map, it sits in the top-left quadrant — mobile-first and specialist — alongside Starling and Monzo, but with a tighter product focus. On the Human Touch vs. Automation map, it occupies a genuinely unique position: niche-focused and human-led, a quadrant no other competitor holds with conviction.

That human-led, niche-focused position is both Zempler’s greatest asset and its most underutilised one. The brand serves 650,000+ businesses, has accumulated 9,000+ five-star Trustpilot reviews, and offers a Business Creditbuilder product that has no direct equivalent across all fourteen competitors analysed. Yet its current positioning — “simpler banking for self-starters” — competes directly with the contested territory that Starling, Monzo, and Tide have already saturated.

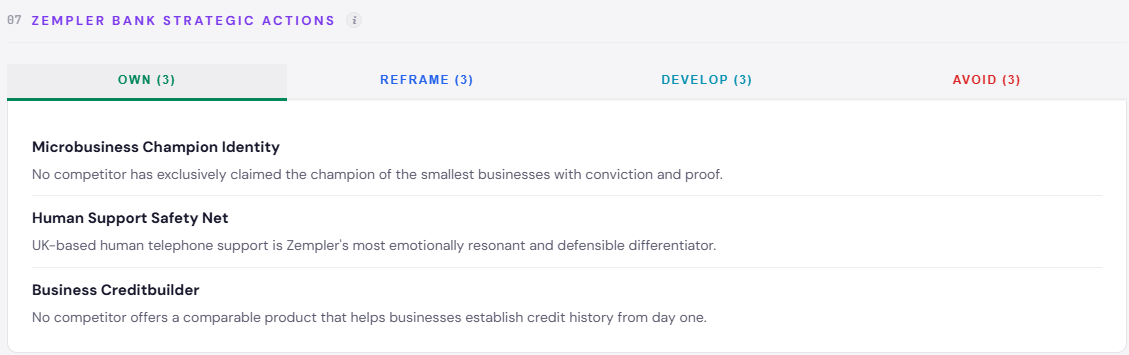

Three unoccupied territories sit within Zempler’s reach. “The Microbusiness Champion Bank” — the exclusive champion of the smallest businesses, with proof — is unclaimed. “Banking with a Human Safety Net” — making human telephone support the central brand promise rather than a feature footnote — is unclaimed. “The Bank That Builds Your Credit” — owning the Business Creditbuilder as a category-defining product — is unclaimed. Zempler has the evidence to claim all three. The question is whether it will.

The Competitive Dynamics Nobody’s Talking About

The obvious threat is the Critical triad. Starling, Monzo, and Tide are well-resourced, well-reviewed, and well-positioned for the broad SME market. But they are also broad — their scale means they cannot credibly claim to champion the smallest businesses without diluting their mass-market appeal. This is the structural gap Zempler can exploit.

The less obvious threat is the automation race. ANNA Money’s AI Auto Accountant and Countingup’s SmartTax AI are winning the niche-focused, automation-heavy quadrant — the same audience Zempler serves. If AI-assisted bookkeeping and tax filing become table stakes for microbusiness banking, Zempler’s human-first model risks being perceived as a gap rather than a choice. The risk is not that Zempler loses customers to Starling — it’s that it loses the next generation of sole traders to ANNA Money, who promise to handle the admin entirely.

What if Starling or Monzo decided to explicitly target the microbusiness segment with a dedicated sub-brand or product line? Their existing scale and brand recognition would make them formidable. The window for Zempler to claim the microbusiness champion territory is open now — but it won’t stay open indefinitely. The longer Zempler positions as “another simpler banking option,” the harder it becomes to credibly claim the champion identity once a better-resourced competitor decides to occupy it.

What This Means: Strategic Implications

The one move that matters most is a positioning pivot from feature to persona. Zempler’s current messaging competes on what it offers (simpler banking, free account, built-in tools) rather than who it serves (crafters, grafters, self-starters who need a bank that champions them). The data supports a much bolder claim: Zempler is the only fully regulated UK bank with human telephone support, Post Office cash deposits at 11,500 locations, and a dedicated credit-building product — a combination no competitor can replicate.

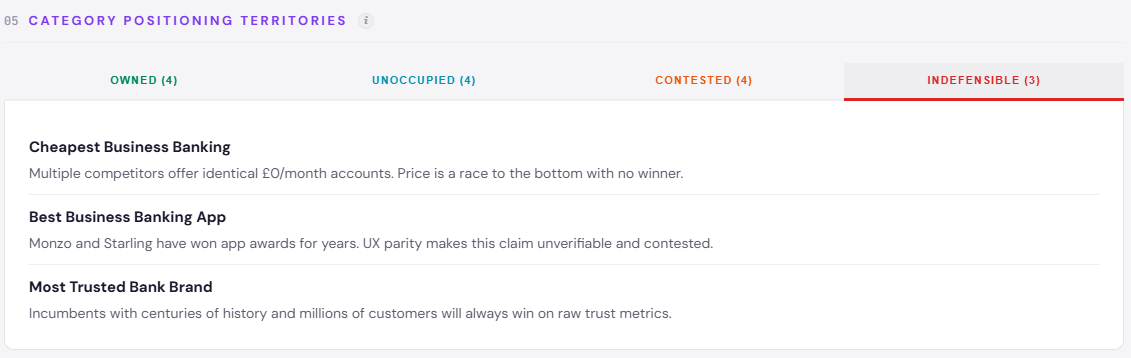

What to stop doing: competing on “simpler banking” and “free account” as primary claims. Both are contested to the point of meaninglessness. Starling, Monzo, Tide, Mettle, and Virgin Money all offer free accounts. All claim simplicity. Zempler’s free tier is not differentiated by its price — it’s differentiated by what’s included: human support, Post Office access, and built-in tools that work with any accountant’s software.

What to watch: the incumbents. NatWest bundles FreeAgent for free. Lloyds offers 12 months of free banking. If the Big Four continue bundling software and extending introductory offers, the “free account with tools” narrative loses its edge. Zempler’s most durable defence is the combination that no digital-only competitor can match: regulated, human, and physically accessible. That combination should be the headline, not the footnote.

This is a converging market — the window for differentiation is narrowing as challengers consolidate messaging and incumbents bundle features. The urgency is real.

The Bottom Line

Zempler Bank is not another digital challenger. It is a regulated UK bank with a human safety net, a unique credit-building product, and 650,000+ microbusinesses who already chose it. The positioning landscape says the same thing the data says: the territory is open, the evidence is there, and the only thing missing is the claim.

Explore the full Business Banking positioning landscape for Zempler Bank - interactive competitor analysis, territory maps, and strategic actions: available here

This analysis was produced using THEO Growth — positioning intelligence for brand strategists. If you work with brands and need competitive positioning analysis, see how it works.